2025 marked another year of significant financial and strategic accomplishments for Basilea. Cresemba continues to deliver strong in-market sales growth, and although it is maturing in the key markets of the US and Europe, it is important to remember that Cresemba is marketed in 76 countries. It is still relatively early in its product life cycle in Japan and China, two significant markets. Nevertheless, the market is beginning to look beyond Cresemba, also reflected in management’s recently announced Agenda 2030, given its expected loss of exclusivity in the US from September 2027 and potential generic competition in Europe in H2 2028. With the novel antifungal fosmanogepix progressing through pivotal Phase 3 trials, the long-term outlook for Basilea’s antifungal franchise looks highly promising. The late-stage pipeline was also boosted in 2025 with the addition of the Phase 3-ready combination antibiotic, ceftibuten-ledaborbactam, targeting the large market opportunity of complicated urinary tract infections (cUTI) and particularly those caused by problematic Gram-negative Enterobacteriaceae. We believe peak sales could be approximately $450m with potential approval in 2029.

Fosmanogepix looking good

We remain highly enthusiastic about the prospects for fosmanogepix. Not only does it have the potential to have a much broader label than Cresemba, assuming success from ongoing Phase 3 trials in invasive candidiasis (FAST-IC) as well as invasive moulds (FORWARD-IM), it possesses activity against most of the priority pathogens highlighted by WHO. The Phase 3 programme is largely funded by BARDA, and we look forward to the data readouts from both trials in 2028. Based on its profile and clinical data, we forecast fosmanogepix could generate peak sales of around $1.2bn, comfortably exceeding those of Cresemba. Furthermore, its use in expanded access programmes has also provided an additional insight into its activity targeting problematic (life-threatening) fungal infections in a real-world setting. The importance of fosmanogepix has been reflected in FDA conferring QIDP and Fast Track status in invasive aspergillosis (IA), candidiasis, scedosporiosis, fusariosis, cryptococcosis, coccidioidomycosis and mucormycosis, suggesting an accelerated regulatory process.

Multiple growth drivers to bridge the gap

2026 should provide an insight into the US sales progress of Zevtera, principally in the bacteraemia (SAB) indication through licensee Innoviva Specialty Therapeutics (IST). Leading indicators continue to look good, and we forecast peak sales of $380m. Following on behind fosmanogepix is BAL2062 which looks to be an important treatment option in the IA indication. Additionally, the earlier stage pipeline contains the potential Gram-negative antibiotic BAL2420 targeting LptA which recently entered Phase 1. Importantly, a large part of the development cost of these programmes is facilitated by non-dilutive BARDA (BAL2062) and CARB-X (BAL2420) funding.

Bridging the gap

The 2025 full year results from Basilea took the opportunity to remind us of the steps already taken by the company not only to rejuvenate its anti-infectives franchise but also to provide an insight into the measures already underway as the company transitions through the loss of exclusivity for Cresemba, its lead revenue generator through Agenda 2030.

While Cresemba will clearly be a difficult act to follow, we believe that the company is in a strong position with Zevtera recently launched in the US and two late-stage programmes already partially de-risked. Overall, our forecasts suggest peak end market sales of circa $1.2bn for fosmanogepix (which compares to Cresemba’s current sales of $693m), $380m for Zevtera and $450m for ceftibuten-ledaborbactam. Importantly, all three should be on the market in the 2030 timeframe. The other positive aspect of Agenda 2030 is the expectation of continued strong cashflow generation from Cresemba and Zevtera of circa CHF600m between now and 2030.

Late-stage pipeline progressing

Source: Basilea investor presentation

Given the strength of the new anti-infectives pipeline and the demonstrably successful track record in delivering new high-value assets, we continue to believe that Basilea remains on track to become a leading anti-infectives powerhouse. With a rejuvenated late-stage pipeline, the company looks set to reap the rewards of the various initiatives that have been put in place to highlight the risk of problematic priority pathogens.

We have previously highlighted the importance of WHO’s efforts to raise awareness of fungal infections, but it is also worth mentioning the efforts by CDC with respect to Candida (March 2022) and BARDA’s new priority (in 2022) to advance development of novel antifungals. BARDA has proven to be a rich vein of non-dilutive funding for the company extending beyond the Other Transaction Agreement (fosmanogepix and BAL2062) to the development of Zevtera in the US as well as ceftibuten-ledaborbactam.

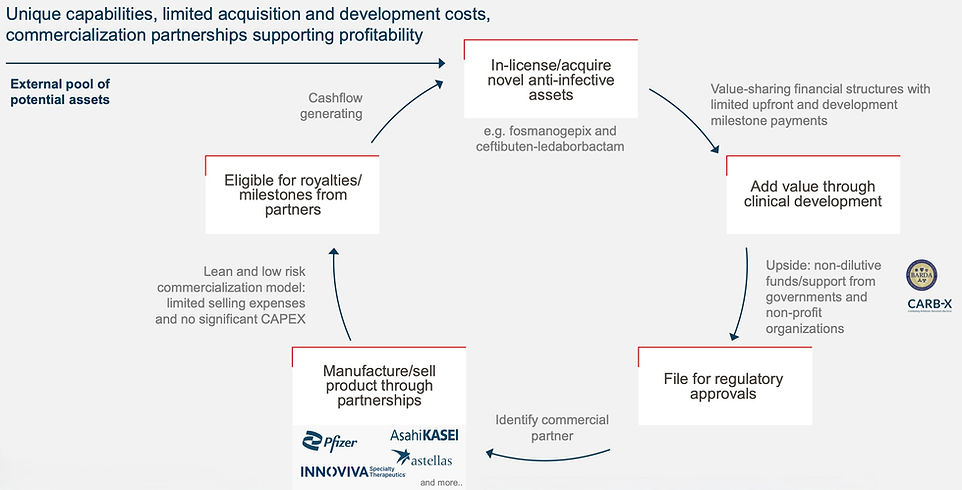

Basilea has benefited from a proven business model and a successful track record, having shown its prowess in identifying novel drug candidates either in-house (the company was originally a Roche spin-out) or increasingly through in-licensing or acquisition efforts. The company then adds considerable value de-risking programmes, undertaking clinical development and filing for regulatory approval.

We believe that this model represents a very attractive aspect of the investment case and is a key differentiating feature from its peers. One of the main elements behind the company’s financial success has been attracting and securing relevant commercial partners.

Proven business model

Source: Basilea investor presentation

While much of this has been funded by the success of antifungal Cresemba, through heavyweight partnerships with Astellas (US) and Pfizer (most of Europe and Asia), Basilea has been extremely successful in securing non-dilutive funding principally from BARDA.

BARDA funding has facilitated the continued clinical development of Zevtera and ceftibuten-ledaborbactam in the key US market, as well as providing 60% of the funding for antifungals fosmanogepix and BAL2062. With a focus on developing anti-infectives that target problem pathogens highlighted by bodies such as WHO, BARDA remains an important source of funding. The award of a multi-year Other Transaction Agreement (OTA) of up to $268m in 2024 is testament to the importance of the anti-infective programmes at Basilea.

This virtuous cycle of funding looks set to continue, we believe, given the existence of the OTA and the flexibility that this provides to Basilea as it deepens and progresses its anti-infectives pipeline. Basilea has suggested that it aspires to have four commercial-stage assets by 2030. Given its track-record in successfully executing on its business model, we believe that Basilea will be viewed as a partner of choice by those looking to partner their anti-infective programmes.

All thanks to Cresemba

The financial performance of Cresemba has provided the cash to allow the company to re-populate its anti-infective pipeline. Success has also come from the company’s expertise, epitomised by its focus on unmet medical needs and perhaps also its position as a likely partner of choice for many smaller anti-infectives companies.

This focus on critical pathogens appears to be well aligned with endeavours by health bodies such as WHO to increase awareness of the anti-infective challenges facing humanity. For example, we have previously highlighted the publication in 2022 of a list of critical fungal infections which has significantly increased the profile and industry participation in the development of novel antifungal treatments.

WHO fungal priority pathogens list

Source: World Health Organization

Securing a multi-year Other Transaction Agreement (OTA), which provides up to $268m of funding over up to 12 years, represented a key transformational event for the company. BARDA utilises OTAs to “…foster innovation and promote collaboration.” They are a key element of the US government's preparedness for various threats, including, in the case of Basilea, emerging infectious disease threats.

Fosmanogepix to the fore

The more clinical (mostly real-world) data published on fosmanogepix the more enthusiastic we have become. As the first from the new ‘gepix’ class, fosmanogepix (a prodrug of manogepix) inhibits fungal cell wall synthesis by targeting GPI-anchored protein maturation by inhibiting Gwt1 in the GPI biosynthesis pathway. Despite its evolutionary conservation, there are significant differences in the GPI pathway between humans and other organisms, enabling the development of inhibitors with excellent selectivity. This apparent selectivity has been borne out in the clinical studies confirming its benign safety profile.

Preclinical and clinical data suggest that fosmanogepix has a differentiated and highly relevant profile. It has high bioavailability (>90%), providing the potential for both oral and intravenous (IV) preparations. This is relevant to the extent that the echinocandins can only be delivered by the IV route. The importance of echinocandins lies in their role as the first-line treatment for Candida auris infections, where increasing resistance to the azoles has become a growing concern.

We believe that fosmanogepix, with its broad-spectrum activity against almost all priority pathogens, including resistant fungal infections, suggests that peak sales should comfortably exceed those of Cresemba. As we highlighted previously, C. auris and Nakaseomyces glabrata have recently proven to be problematic fungal infections in the US. Moreover, fosmanogepix post-approval should possess a much broader label than Cresemba. Importantly, fosmanogepix has also demonstrated activity against other rare, difficult-to-treat moulds that were typically resistant to other antifungal agents including Aspergillus resistant to echinocandins and fluconazole.

The broad spectrum and potency of fosmanogepix have been demonstrated in various animal models. Several key attributes have been confirmed, including its ability to reduce fungal burden, particularly in key organs such as the brain, where the echinocandins have negligible activity. Overall, fosmanogepix has a good volume of distribution, penetrating many important tissues and organs, including liver, lung, and eye. As a novel first-in-class antifungal, resistance to fosmanogepix should be a distant concern in a real-world environment.

Fosmanogepix’s clinical development

Three Phase 2 studies were completed in patients with candidaemia, including those caused by C. auris and invasive mould infections. C. auris has been associated with high mortality rates (circa 60%) in patients hospitalised with a C. auris infection. Resistance to existing classes of antifungals has been a characteristic of almost all C. auris strains. The rapid emergence of C. auris, with its multidrug resistance and associated high mortality rate, has led various health authorities to highlight it as a fungal infection of significant concern. In the US, the CDC has highlighted the increasing prevalence of C. auris infections. Consequently, the CDC has designated C. auris as an urgent antimicrobial resistance threat in the US. In March 2023, the CDC issued a warning regarding the increasing risk of infection from drug-resistant C. auris following a spike in cases in California.

Phase 3 in progress

Reflecting the unmet need and the commercial opportunity, the two Phase 3 trials comprise one targeting candidaemia/invasive candidiasis, and a second targeting invasive mould infections.

Global phase 3 study in invasive candidiasis

Source: Basilea investor presentation

Global phase 3 study in invasive mold infections

Source: Basilea investor presentation

The first Phase 3 study, Fosmanogepix Against Standard-of-care Treatment in Invasive Candidiasis (FAST-IC), was initiated in September 2024. This study is a global, randomised, double-blind trial designed to demonstrate non-inferiority to the standard of care. The trial aims to enrol 450 patients and will compare fosmanogepix to caspofungin, both of which offer oral step-down options. The primary endpoint agreed with FDA is 30-day survival, while for EMA approval, the primary endpoint is overall response at the end of study treatment.

The invasive mould (FORWARD-IM) study is an open-label, randomised trial, and is expected to enrol approximately 220 patients. The study aims to compare fosmanogepix versus best available therapy (BAT) against a broad range of clinically and commercially relevant invasive fungal infections, including Invasive aspergillosis (IA), Fusarium spp., Scedosporium spp., Mucorales, Lomentospora prolificans, as well as other multi-drug-resistant moulds. This study was initiated in July 2025. Given that fosmanogepix has obtained Fast Track status from FDA for seven different fungal infections, we believe that it will be relevant to a broad range of critical fungal pathogens.

The use of expanded access programmes (EAP) has markedly increased early access to important new therapies. We have been greatly encouraged by the extent fosmanogepix has been used and the quality of the data generated. Given the increasing threat from fungal infections, particularly with respect to increasing resistance we believe that the totality of the data from the controlled clinical trials and the EAPs will provide a very large and compelling insight into fosmanogepix’s potential. Moreover, these data should help to attract a suitable partner as well as commercialisation efforts, suggesting the potential for a rapid roll out and uptake.

Broad existing experience with fosmanogepix

Source: Basilea investor presentation

The above diagram demonstrates the excellent applicability of fosmanogepix to a broad range of important fungal infections. While the competitive environment surrounding Candida and Aspergillus may be more intense, the schematic does not include other important differentiating features which favour fosmanogepix. Nevertheless, it is encouraging and reassuring to see that a relatively full pipeline of novel antifungal agents is progressing through clinical development. While olorofim may have been undone initially by following a limited population pathway, we are heartened to see that rezafungin was approved on the back of a relatively small Phase 3 study (with a generous 20% non-inferiority margin).

Olorofim is a member of the ortomide antifungal class targeting fungal dihydroorotate dehydrogenase (DHODH), which is involved in pyrimidine synthesis, and we have previously highlighted its checkered development. Although not a broad-spectrum antifungal, it has broad microbiologic activity against several important invasive moulds. Available orally, olorofim was awarded FDA Breakthrough Therapy Designation for the treatment of invasive fungal infections in patients with limited or no treatment options, including aspergillosis refractory or intolerant to currently available therapy, and infections due to Lomentospora prolificans, Scedosporium, and Scopulariopsis species, as well as treatment of patients with coccidioidomycosis refractory to standard of care.

In May 2022, the originator, F2G, received $100 million in upfront payments, with the potential to receive up to a further $380 million in regulatory and commercial milestones, as well as double-digit sales royalties from its commercial partner, Shionogi. However, olorofim received a complete response letter from FDA in June 2023 following its application for approval with a proposed label for the treatment of invasive fungal infections in patients with limited or no treatment options. More encouragingly, the outlook for the progression of olorofim took a significant step forward with the announcement that F2G had raised $100m to fund additional Phase 3 evaluation.

Results from the Phase 2b study were published in The Lancet Infectious Diseases in 2025. This was a single-arm, open-label study that enrolled 204 patients with few or no treatment options (including azole resistance) over 22 centres in 11 countries. 28.7% of treated patients met the primary endpoint of successful global response at day 42. More encouragingly, when patients with stable disease were included, the response rate increased to a more impressive 75.2%. These results are important to the extent that many of the infections were resistant to existing therapies. Overall, the trial included patients with invasive aspergillus (n=101), Lomentospora prolificans (n=26), Scedosporium (n=22) and Coccidioides (n=21).

Ibrexafungerp (SCY-078) represents the first of a new class of “fungerps”. Although the “fungerps” may share the same mechanism of action as the echinocandins they target a different binding site in the fungal cell wall (a derivative of enfumafungin). Its mode of action increases the permeability of the fungal cell wall, ultimately resulting in cell death.

Ibrexafungerp displays fungistatic activity against Aspergillus and fungicidal activity against Candida but lacks reliable activity against Fusarium or Mucorales. Originator Scynexis partnered ibrexafungerp with GSK with approval (as Brexafemme) in 2021/22 for vulvovaginal candidiasis (VVC) and its recurrence (RVVC).

Given a general lack of cross-resistance with the echinocandins and its availability as an oral presentation, there is the potential for ibrexafungerp to be used as an oral step-down therapy to injectable echinocandins in the short term. With respect to potential direct competition to fosmanogepix, we note that the Phase 3 study (MARIO) with ibrexafungerp as a step-down therapy in the treatment of invasive candidiasis has been terminated as resolution to a disagreement between Scynexis and GSK.

The antifungal focus at Scynexis has moved to its second-generation “fungerp” SCY-247 which is also available in injectable and oral presentations. Earlier stage still, Scynexis is also pursuing the potential of several next generation “fungerps”, suggesting an extended pipeline of novel anti-fungals.

SCY-247 appears to have potent activity against a broad range of fungal infections, including multi-drug-resistant strains, such as multi-drug-resistant C. auris and Aspergillus spp. If successful, SCY-247 could capitalise on the use of the echinocandins as first-line treatment options in invasive fungal infections caused by Candida and Aspergillus. SCY-247 exhibits activity against resistant strains and appears more potent (with greater bactericidal activity) than ibrexafungerp against resistant strains of C. auris. We also note its differentiated activity against N. glabrata, including strains that possess resistance to echinocandins.

Undoubtedly, the profile of SCY-247 appears promising and could present another important addition to the physicians’ armamentarium targeting problematic fungal infections. SCY-247, however, remains at an early stage of development with a Phase 2 study in invasive candidiasis anticipated to begin in 2026. Unlike fosmanogepix, this programme has not (yet) been endorsed with non-dilutive funding, and we note that Scynexis completed 2025 with a limited cash balance of $37.9m.

Rezafungin rounds out the near-term competitive environment. Rezzayo (rezafungin) is a novel echinocandin (derived from anidulafungin). Its main differentiating features include a longer half-life, allowing for once-weekly intravenous dosing, a better volume of distribution, and activity against biofilms and azole-resistant Candida, including C. auris and N. glabrata. The pharmacokinetic profile of rezafungin facilitates a front-loading dosing regimen with a higher loading dose administered. This regimen results in high exposure early in patient treatment, resulting in increased fungal killing. Rezafungin should benefit from the echinocandins' position in guidelines as first-line treatment, and its once-weekly dosing should facilitate outpatient treatment, potentially removing the need for a central venous line. Rezafungin also offers greater stability than other echinocandins and represents a significant advance over existing members of the class.

Rezafungin was approved in the US in March 2023 for the treatment of adults with candidemia and/or invasive candidiasis who have limited or no alternative treatment options. European and UK approval was secured in late 2023/early 2024. Approval was based on a single Phase 3 trial where rezafungin was compared to caspofungin (followed by oral step-down therapy). The primary endpoint was 30-day all-cause mortality using a 20% non-inferiority margin.

Considering the competitive environment, it is tempting to conclude that if successfully developed, fosmanogepix offers a broader spectrum, encompassing most of the WHO-listed critical fungal infections. Importantly, its excellent penetration of tissues and organs, such as the CNS and eye, where other antifungal approaches are deemed insufficient, promises a significant differentiation. It also offers the potential for oral step-down therapy, which could be a meaningful differentiator given that it’s the same treatment. In contrast, oral step-down therapy in invasive candidiasis with an echinocandin usually involves moving to azole-based treatment.

Looking for increased Zevtera momentum

As a 5th-generation cephalosporin antibiotic with anti-MRSA activity, the commercial appeal of Zevtera (ceftobiprole) may initially appear limited, particularly given the long-term availability of ceftaroline, another 5th-generation cephalosporin. While ceftaroline has found use (off-label) to treat Staphylococcus aureus bacteraemia (SAB), we believe there was a clear need for compelling data from a prospectively designed clinical trial to confirm the activity and relevance of this class in the treatment of SAB, particularly where MRSA is involved.

It is clear that despite Zevtera’s broad label, it is the SAB indication which is key to Zevtera’s future commercial success and has been reflected in the attraction of Innoviva Specialty Therapeutics (IST) as the US commercial partner for Zevtera. This is a substantial opportunity with circa 120,000 SAB patients in the US per year, of whom approximately half involve infection with MRSA. With only vancomycin and daptomycin approved for SAB and with a growing threat of emerging resistance, there is a clear need for new treatment alternatives, particularly one with the known safety and tolerability profile associated with the cephalosporin class.

We have previously noted the lack of up-to-date treatment guidelines and the existing practice variation in the treatment of SAB, perhaps reflecting the lack of treatment options and compelling clinical data from well-controlled trials (until ERADICATE). We look forward to the widely anticipated new IDSA/ESCMID treatment guidelines expected later in 2026 which we anticipate could be fortuitous timing for Zevtera given its roll out in the key US market. For now, treatment with a beta-lactam antibiotic remains first line for patients with susceptible infections (MSSA), which can last up to six weeks if the condition has become metastatic, compared to two weeks if the bacteraemia remains uncomplicated. Antibiotics typically used for MSSA include anti-Staphylococcal penicillins such as flucloxacillin and first-generation cephalosporins such as cefazolin.

Patients with confirmed and suspected MRSA, as well as in institutions where resistance is a concern, look to be the initial unmet need for Zevtera. MRSA inevitably leads to poorer outcomes, with 15%-50% mortality rates in patients with MRSA bacteraemia. The glycopeptides, vancomycin and daptomycin, are first-line treatments in MRSA bacteraemia, requiring 4-6 weeks of intravenous therapy. Metastatic infections often require surgical intervention and can result in extended hospitalisation.

Although still relatively rare, there is a growing risk of resistance to both vancomycin and daptomycin to the extent that combinations offering synergistic activity have been evaluated including daptomycin + ceftaroline and daptomycin + fosfomycin. More promisingly, the lipoglycopeptide dalbavancin has also been used (off-label) as an alternative to vancomycin-resistant infections and has the added benefit of offering a lower level of renal injury in comparison and a long half-life, resulting in a much-reduced dosing schedule. Dalbavancin appears to us to be an attractive alternative proposition offering the potential for a shorter and less invasive treatment regimen, lowering risks associated with prolonged central venous access.

The long-awaited and much-anticipated publication of the Phase 2b DOTS (dalbavancin as an option for treating SAB) study finally appeared in the August 2025 issue of JAMA. As noted above, dalbavancin has been used off-label for the treatment of complicated SAB, with the results first presented at ESCMID in April 2024. Although dalbavancin did not meet the primary endpoint of superiority to standard of care as measured by the highly relevant (for dalbavancin) desirability of outcome ranking (DOOR), which looked at a combination of clinical success, infectious complications, safety complications, mortality and health related quality of life, it did meet the secondary outcome of non-inferiority to standard of care with respect to overall clinical success. The formal publication of DOTS in a prestigious journal should help raise awareness of the importance of new and alternative approaches to treating SAB, particularly as they relate to achieving better outcomes.

The standard of care (vancomycin and daptomycin) has been associated with a significant risk of treatment failure. Furthermore, vancomycin has poor tissue distribution and a risk of renal toxicity. Additionally, daptomycin is inactivated in the lungs, rendering it ineffective for the treatment of respiratory infections. Ultimately, we believe there is a clear need for additional antibiotics in SAB with a notable shortage of high-quality controlled studies. Previously, salvage therapy using an unapproved (off-label) antibiotic (such as the 5th generation cephalosporin ceftaroline) has proven to be a last resort approach in those with a persistent infection.

The attraction of (IST) brings a committed partner for the US commercialisation of Zevtera. We believe there are several reasons why the attraction of IST represents a committed partner, which should help maximise Zevtera’s peak sales potential. The current anti-infective portfolio at IST comprises several hospital-based complementary antibiotics targeting important infectious diseases. Although Zevtera, as a 5th-generation cephalosporin, may not represent a transformative approach, considering the long-term availability of other similar treatments, such as ceftaroline, it is the only cephalosporin to have a specific approval for SAB.

IST has clearly recognised the need and market potential associated with the SAB opportunity, and we remain heartened by positive leading indicators, which include hospital formulary acceptance and repeat orders from large hospitals. With this growing awareness and presuming that Zevtera finds its place in the new treatment guidelines when they emerge, we anticipate (and as Basilea has alluded to) growing sales momentum later this year.

Previously, we modelled Zevtera to achieve a 10-12% peak penetration of the US bacteraemia market, resulting in a peak sales opportunity of $250m. Patients with SAB typically receive antibiotics for a duration of 2 to 6 weeks. Additionally, we have assumed that Zevtera can secure a modest 2-3% share of the large ABSSSI market at peak, recognising that this is a much more competitive area with other more entrenched competitors (e.g. ceftaroline). Nevertheless, given the size of the ABSSSI indication in the US, even this modest market penetration suggests a peak sales market potential of $130 million, and we also have the CABP indication to consider. Overall, we forecast that ceftobiprole could achieve peak in-market sales of approximately $380 million in the US.

Ceftibuten-ledaborbactam strengthening Phase 3 pipeline

Resistance associated with Gram-negative infections is particularly concerning, with few treatment options available and little progress. Such is the seriousness of AMR that the WHO has published a list of priority pathogens, the majority of which are Gram-negative. The list is divided into three priorities based on their risk to human life. The highest-level Priority 1 pathogens are all Gram-negative and are deemed to pose a critical threat and comprise Acinetobacter baumannii, Pseudomonas aeruginosa and Enterobacteriaceae, where resistance has become a significant problem. This priority list as described by WHO is relevant to the extent that it clearly identifies the unmet need and has been an important indicator of the attractiveness of these development programmes to deliver non-dilutive funding from relevant and deep-pocketed organisations like BARDA.

This is directly relevant to the addition of the ceftibuten-ledaborbactam etzadroxil combination to the late-stage development pipeline. Ceftibuten is an orally available 3rd generation cephalosporin antibiotic originally approved as Cedax for susceptible strains of bacteria, including Moraxella catarrhalis (including beta-lactamase producing strains), Haemophilus influenzae (including beta-lactamase producing strains) and Streptococcus pneumoniae as they relate to acute bacterial exacerbations of chronic bronchitis, acute bacterial otitis media, and pharyngitis/tonsillitis caused by Streptococcus pyogenes. Ledaborbactam etzadroxil is a novel, broad-spectrum boronic acid beta-lactamase inhibitor.

The intention is to develop the combination as an oral therapy for the treatment of cUTIs caused by Enterobacterales. Enterobacterales remain the principal cause of most uncomplicated and complicated UTIs, with cystitis, for example, a common reason for prescribing antibiotics, generally with beta-lactam antibiotics, the favoured first-line treatment option given their benign profile and potent bactericidal activity. As a result of widespread prescribing for various indications, resistance has become a significant issue. This has been a long-standing concern which began with co-trimoxazole, almost 20 years ago, followed by resistance to fluoroquinolones, followed by the cephalosporins. Ceftibuten-ledaborbactam is active against multi-drug-resistant pathogens including extended-spectrum beta-lactamase (ESBL) producers and carbapenem-resistant Enterobacterales (CRE). The relevance of the combination in treating cUTIs is reflected in the granting of QIDP and Fast Track designations by the FDA.

UTIs caused by extended-spectrum beta-lactamase-producing Enterobacterales have become a growing issue in many countries, with resistance to fluoroquinolones as well as oral beta-lactams such as cephalosporins and amoxicillin-clavulanate, and carbapenems. The emergence of carbapenem resistance is particularly concerning given its association with increased mortality, further highlighting the need for new treatment options. Oral fluoroquinolones, for example, are no longer recommended as empiric therapy for cystitis given the threat of increasing resistance. Moreover, patients with pyelonephritis (kidney damage) have few treatment options, given growing concerns over resistance to oral fluoroquinolones.

First line empiric therapy of cUTI as per IDSA guidelines suggests the use of 3rd or 4th generation IV cephalosporins, and that where an oral route of treatment is suitable, the fluoroquinolones or trimethoprim-sulfamethoxazole is appropriate or as an alternative to oral cephalosporins. The oral activity of the ceftibuten-ledaborbactam combination should therefore be appropriate for cUTI patients as an oral step-down therapy for those who have completed several days of intravenous therapy.

This programme follows the same tried and tested route to reverse the resistance to other beta-lactam antibiotics, including ceftazidime-avibactam (Avycaz/Zavicefta), imipenem-relebactam (Recarbrio), meropenem-vaborbactam (Vabomere), and ceftolozane-tazobactam (Zerbaxa), with other similar programmes in development.

The success of Avycaz in particular portends well for the potential future commercial success of ceftibuten-ledaborbactam, we believe. Avycaz is a combination of the 3rd generation cephalosporin ceftazidime and a novel beta-lactamase inhibitor. Ceftazidime was chosen at the time, given its broad beta-lactamase spectrum, making it a better treatment option for multidrug-resistant bacteria. Avycaz was approved in 2015 for complicated intra-abdominal infections (cIAI) and in 2017 for cUTI (including pyelonephritis) caused by susceptible Gram-negative bacteria, including Enterobacteriaceae and P. aeruginosa. The third approval for HAP/VAP was provided in 2018. Avycaz generated sales of $659 million in 2024. While clearly benefiting from a broader label than ceftibuten-ledaborbactam, the latter has the benefit of being an oral preparation, offering outpatient and oral step-down treatment options for cUTI patients. According to the CDC, there are approximately 3 million patients in the US every year suffering from a cUTI, with 600,000 hospitalisations, the majority of whom are female. With an approximate cost of $7500-$15000 for 7/14 days of treatment, even a modest 10% share of the hospitalised market suggests peak sales of $450m in the US alone. It is also worth noting that there are approximately 250,000 patients with pyelonephritis in the US, confirming the magnitude of the current unmet need.

Given the scale of the unmet need and the size of the opportunity, efforts are ongoing to develop new oral approaches to treat cUTIs, in addition to the ceftibuten-ledaborbactam combination. That said, there have also been notable failures with eravacycline, a once heavily touted new approach, failing to show non-inferiority to ertapenem. More positively, the oral carbapenem tebipenem HBr for the treatment of cUTIs is approaching approval in the US following the positive outcome of the Phase 3 PIVOT-PO study. If approved, tebipenem would represent the first approval of an oral carbapenem for the treatment of cUTI in the US.

Although tebipenem should be the first to market, we note that as a new entrant from an existing class, there is a potential concern that class-specific cross-resistance may emerge over time, suggesting a need for multiple treatment options. Moreover, ceftibuten-ledaborbactam may also offer the potential benefit of a lower pill burden and less frequent dosing (OD) than tebipenem (2x 300mg every six hours) and a differentiated microbiological profile (no reduced activity against carbapenem-resistant Enterobacteriaceae), suggesting that it should offer a highly relevant addition, despite the expected availability of tebipenem. Further evidence of the remaining unmet need has been the award of substantial funding from BARDA initially for Venatorx now transferred to Basilea.

We have described ceftibuten-ledaborbactam as a validated programme based mainly on the preclinical data during its tenure at originator Venatorx, as well as the successful development of other existing beta-lactam antibiotics with new beta-lactamase inhibitors. Several studies have examined and compared the activity of ceftibuten-ledaborbactam against relevant Enterobacteriaceae clinical isolates, including non-susceptible clinical isolates. In the most recent study, ceftibuten-ledaborbactam was tested against a large number (3889) of relevant (recent and global isolates), which included those with extended beta-lactamase activity, multidrug resistance and other non-susceptible organisms. Given the mix of different (and difficult to treat) isolates tested and the anticipated activity of ledaborbactam, the study confirmed the ability of the combination to restore ceftibuten activity with susceptibilities similar to newer parenteral combinations (imipenem-relebactam), building on previous studies confirming similar activities to other newer parenteral beta-lactamase combinations such as ceftazidime-avibactam and meropenem-vaborbactam. For us, the result against multidrug-resistant isolates of almost 90% (89.7%) susceptibility was particularly impressive and compares well to 98.3% of isolates, which were presumed to have an extended beta-lactamase activity.

Ceftibuten-ledaborbactam arrived at Basilea with successful preclinical and Phase 1 data. This is a Phase 3-ready asset and we note that there are ongoing discussions with regulatory agencies with respect to the final design of the Phase 3 programme. According to the company, the current expectation is that the programme would likely compare ceftibuten-ledaborbactam to an IV carbapenem starting in early 2027. For comparison, it is noteworthy that the tebipenem Phase 3 PIVOT-PO study comprised 1687 patients in a non-inferiority design (10% NI margin) comparing oral tebipenem to IV imipenem-cilastatin. PIVOT-PO was stopped early for efficacy following a pre-planned interim analysis to assess efficacy and futility. Overall response at test of cure (primary endpoint) was 60.2% in the tebipenem compared to 58.5% in the active control arm.

BAL2420 – a novel Gram-negative candidate

BAL2420 represents another programme targeting Gram-negative infections, but in a highly targeted fashion in line with current guidelines of antibiotic stewardship. It is, however, earlier in development than the ceftibuten-ledaborbactam combination entering Phase I evaluation in March 2026.

BAL2420 targets LptA with the objective of disrupting the outer membrane of Gram-negative bacteria by targeting the lipopolysaccharide (LPS) bridge. Given the outer membrane’s importance in preserving the integrity of Gram-negative bacteria, targeting LPS production and its transport machinery has proven a productive approach in antibiotic drug development. Nevertheless, apart from the polymixins and colistin, which have significant limitations, efforts to develop direct inhibitors of LPS have been found wanting so far. Given the heightened risk of kidney damage associated with colistin and Polymyxin B, they are generally regarded as last-resort treatment options. The preclinical profile of BAL2420 appears to be very appealing as a potent inhibitor of LptA, exhibiting rapid bactericidal activity. Notably, it shows activity against Enterobacteriaceae strains (WHO Priority 1), including those resistant to beta-lactams and colistin.

Despite its relatively early stage of development, we believe the award of non-dilutive funding from CARB-X is a significant endorsement of this approach, as CARB-X focuses on accelerating programmes targeting the WHO and CDC’s priority pathogens list. CARB-X interest reflects the importance of LptA and BAL2420 as an exciting novel approach to targeting insidious and life-threatening infections caused by Enterobacteriaceae. We look forward to supportive data now that BAL2420 has entered clinical trials. Currently, BAL2420 is not included in our financial model or valuation of Basilea.

BAL2062 – a differentiated approach

BAL2062 is the first of a new class of siderophore-like hexapeptide antifungal agents. BAL2062 is differentiated by its novel mechanism of action that includes rapid fungicidal activity, with data generated to date suggesting activity against a range of difficult-to-treat fungal pathogens (including azole-resistant strains). The rapid reduction in fungal burden, along with a lack of cross-resistance to existing antifungal classes (such as the azoles), could be highly attractive features of BAL2062.

BAL2062 originated at Astellas and is a naturally derived cyclic hexapeptide from the Malaysian leaf litter fungus. Its mechanism of action is based on the use by fungi (and other pathogens) of the siderophore ferrichrome. Fungi require ferrichrome to scavenge for essential iron when levels are low. Importantly, it is transported in fungal cells by the Sit1 transporter. Fortunately, since human cells do not possess a Sit1 transporter, BAL2062 is expected to have minimal toxicity.

Although the principal commercial target is likely to be invasive aspergillus infections, including azole-resistant, BAL2062 also has activity against other important fungal pathogens, including N. glabrata and Fusarium solani.

BAL2062 is still in its early stages of clinical development, with Phase 1 clinical evaluation demonstrating its safety and tolerability. BAL2062 also benefits from QIDP and Fast Track designations for IA. Regulatory discussions are currently underway to define its remaining clinical development pathway. The addition of BARDA funding under the existing OTA should help accelerate development if BAL2062’s attractive profile warrants further investigation.

Risks

Basilea's business model currently involves partnerships and out-licensing to third parties, suggesting little influence over sales performance. Nevertheless, execution on key product Cresemba has been excellent through highly appropriate partners (particularly Astellas and Pfizer), and we believe this model has worked well for Basilea and its partners. In particular, these are profitable relationships immediately post commercialisation without Basilea having to bear the significant costs required to launch a new product.

Fosmanogepix is key to the long-term future of the company’s anti-infectives aspirations. The clinical data to date have been supportive and, with positive EAP results, suggest that the programme has been somewhat de-risked. However, Phase 3 clinical evaluation is ongoing, and we have used a 75% probability of success to reflect the remaining risk.

We believe IST will be a committed and effective commercial partner for Zevtera in the US. Zevtera’s sales progress is important to help offset sales lost from generic competition to Cresemba, expected in the US from Q4 2027 and Europe from H2 2028.

The ceftibuten-ledaborbactam programme looks to be a validated addition with a good susceptibility profile, and as a result, we have introduced sales to our financial model, albeit with a 60% probability of approval. Development of new antibiotics for cUTI hasn’t always been straightforward, and we look forward to details of the planned Phase 3 programme.

The LptA programme is both novel and early stage, suggesting that there is still a very real risk of failure. Therefore, we have not included BAL2420 in our financial model until more compelling data are generated. In any event, we expect Basilea to continue replenishing its pipeline with interesting programmes.

Summary and Financial Review - Agenda 2030

For the first time, Basilea has provided an insight into how life might look after the introduction of a Cresemba generic in the key markets of the US and Europe. At the same time, it is also important to remember that although US Cresemba sales may be impacted by generics from September 2027, Europe will not experience generic competition until H2 2028, with end-market sales expected to continue good growth until then. Also, the company has highlighted the significant commercial potential in Japan, where the market is large and Cresemba remains early in its product life cycle. Our forecasts continue to reflect an expectation of a significant decline in Cresemba sales in the US from Q4 2027 with less of a decline in European sales, partially offset by growth in Japan (and China). Encouragingly, Japan now represents 12% of in-market sales (approximately $83m). We suspect that our Cresemba sales forecast mirror the Agenda 2030 expectations although noting that the company has highlighted several potential events which could result in a better financial outcome. These include later than expected introduction of Cresemba generics and sales from new launches such as fosmanogepix and ceftibuten-ledaborbactam.

Strategically, we believe that Basilea is well placed to transition through the financial impact from Cresemba generics. The launch of the 5th-generation antibiotic Zevtera in the US holds significant sales potential, through highly relevant partner IST. The US represents approximately 89% of Zevtera’s market potential given the higher rates of MRSA. Our peak sales forecast of $380m is largely driven by the bacteraemia indication where treatment options are limited, resistance is increasingly a concern, and Zevtera is the only 5th generation cephalosporin with a specific SAB approval. As we have highlighted previously, leading indicators for Zevtera are highly encouraging with Basilea suggesting increased momentum from Q2 this year.

The top line at Basilea should also receive a significant boost over the next several years as significant BARDA funding is recognised. These include payments for fosmanogepix, BAL2062, ceftibuten-ledaborbactam and other candidates in the future which could attract funding from the existing OTA. With the company expecting to continue its highly successful in-licensing efforts, we are hopeful that these will include additional programmes which satisfy the need to treat priority and problematic pathogens and attract further non-dilutive funding.

That said, much rests on the prospects for key pipeline products fosmanogepix and ceftibuten-ledaborbactam. We believe that there are good reasons to be optimistic for both programmes. Fosmanogepix looks to be an exciting addition to the physician’s armamentarium with activity against most of the priority fungal pathogens highlighted by WHO. Not only has Phase 2 data been supportive, but there is also an increasing weight of real-life data reporting its success in treating life-threatening fungal infections and this is set to continue as the expanded access programme grows. Indeed, we have previously highlighted our expectation that with 430 patients having already received fosmanogepix as part of its EAP, there is the real possibility that more patients will have received fosmanogepix as part of the EAP than in the two Phase 3 trials combined. Additionally, we strongly suspect that continued success will further increase awareness ahead of regulatory action, suggesting an expedited roll out and commercial success. Our forecasts suggest that fosmanogepix could represent a much larger commercial proposition even than Cresemba with a much broader label as well as an increased likelihood of global roll out. As a result, our peak sales forecast for fosmanogepix peak sales of circa $1.2bn which compares favourably to estimated end market sales of $693m for Cresemba. Currently, fosmanogepix is expected to be on the market in 2029.

With the arrival of the combination antibiotic ceftibuten-ledaborbactam, Basilea has another Phase 3-ready programme. We have described this as a validated programme, partly because it follows the same tried and tested route to reverse the resistance to other beta-lactam antibiotics, resulting in significant commercial success and also because of the data generated by originator Venatorx. Given the unmet need in the treatment of cUTI and the need for an oral therapy we believe that even a modest 10% share of the market opportunity should result in peak sales approaching $450m following market entry in 2030.

With a combination of lingering Cresemba sales and with the addition (we have assumed a 25% royalty) from fosmanogepix and ceftibuten-ledaborbactam sales we believe that Basilea is already well prepared to take the company onto the next phase of its ambition to become an anti-infectives powerhouse. Our forecasts assume that after a decline in sales in 2028, sales should rebound returning to previous levels by 2033. Our forecasts also assume that the current high level of R&D spending remains although partially offset by BARDA payments.

While recognising the limitations inherent in forecasting, particularly with respect to the impact of generic competition, our financial model suggests that Basilea should remain a profitable company albeit with a significant decline in 2029F, followed by a rebound in profitability as the full impact of US Zevtera sales along with the expectation of a rapid roll out of fosmanogepix and the addition of ceftibuten-ledaborbactam.

Of the above scenarios, the progress of fosmanogepix is arguably the most important determinant of the future success of Basilea’s anti-infective ambitions. We remain comfortable with our expectation of success given the combination of data from clinical trials and ongoing EAPs. Finally, it is worth remembering its differentiated profile which includes: 1. an IV to oral step-down therapy (providing outpatient treatment options) 2. its activity against most of the fungi on the WHO critical list 3. its activity against resistant strains and 4. good penetration of important organs (particularly CNS). All of the above drives our expectation that fosmanogepix should feature strongly in relevant treatment guidelines while enjoying a more rapid global roll out (than Cresemba) which together drive our circa $1.2bn peak sales forecast.

In the interim, while fosmanogepix cannot compensate for the lost Cresemba sales in 2028/29 time period, there are several events which should, if successful, effectively de-risk the investment case at Basilea. For example, continued positive read outs from the EAPs should increase confidence in a positive outcome from the ongoing Phase 3 fosmanogepix programme. Already, the results of the fusarium patient subset published in NEJM are extremely reassuring. Additionally, we have highlighted the open-label nature of the Phase 3 trial in invasive moulds, suggesting the potential for de-risking as the trial progresses.

Our new forecasts reflect FY ’26 guidance and show our expectation of the impact of key events including likely reduction in Cresemba sales and more importantly, the introduction of fosmanogepix and ceftibuten-ledaborbactam. For now, however, we have not included sales from BAL2062 or BAL2420, as we await more clinical data to gauge likely success. Also, the timing of future milestone commitments as part of the fosmanogepix in-licensing has yet to be detailed. However, Basilea has been adept at managing costs while aggressively pursuing the creation of a world-leading anti-infective franchise.

Basilea Income Statement (CHF' 000)

Source: Calvine Partners Research

Basilea Cash Flow Statement (CHF' 000)

Source: Calvine Partners Research

Basilea Balance Sheet (CHF' 000)

Source: Calvine Partners Research

Disclosures

Calvine Partners LLP is authorised and regulated by the Financial Conduct Authority for UK investment advisory and arranging activities.

This publication has been commissioned and paid for by Basilea Pharmaceutica and, as defined by the FCA, is not independent research. This report is considered a marketing communication under FCA Rules. It has not been prepared under the laws and requirements established to promote the independence of investment research. It is not subject to any prohibition on dealing ahead of the dissemination of investment research. This information is widely available to the public.

This report in the United Kingdom is directed at investment professionals, certified high net worth individuals, high net worth entities, self-certified sophisticated investors, and eligible counterparties as defined by the Financial Services and Markets Act 2000 (Financial Promotion) Order 2000. The report may also be distributed and made available to persons to whom Calvine Partners is lawfully permitted. This publication is not intended for use by any individual or entity in any jurisdiction or country where that use would breach law or regulations or which would subject Calvine Partners or its affiliates to any registration requirement within such jurisdiction or country.

Calvine Partners may provide, or seek to provide, services to other companies mentioned in this report. Partners, employees, or related parties may hold positions in the companies mentioned in the report subject to Calvine Partners' personal account dealing rules.

Calvine Partners has only used publicly available information believed to be reliable at the time of this publication and made best efforts to ensure that the facts and opinions stated are fair, accurate, timely and complete at the publication date. However, Calvine Partners provides no guarantee concerning the accuracy or completeness of the report or the information or opinions within. This publication is not intended to be an investment recommendation, personal or otherwise, and it is not intended to be advice and should not be treated in any way as such. Any valuation estimates, such as those derived from a discounted cash flow, price multiple, or peer group comparison, do not represent estimates or forecasts of a future company share price. In no circumstances should the report be relied on or acted upon by non-qualified individuals. Personal or otherwise, it is not intended to be advice and should not be relied on in any way as such.

Forward-looking statements, information, estimates and assumptions contained in this report are not yet known, and uncertainties may cause the actual results, performance or achievements to be significantly different from expectations.

This report does not constitute an offer, invitation or inducement to engage in a purchase or sale of any securities in the companies mentioned. The information provided is for educational purposes only and this publication should not be relied upon when making any investment decision or entering any commercial contract. Past performance of any security mentioned is not a reliable indicator of future results and readers should seek appropriate, independent advice before acting on any of the information contained herein. This report should not be considered as investment advice, and Calvine Partners will not be liable for any losses, costs or damages arising from the use of this report. The information provided in this report should not be considered in any circumstances as personalised advice.

Calvine Partners LLP, its affiliates, officers or employees, do not accept any liability or responsibility with regard to the information in this publication. None of the information or opinions in this publication has been independently verified. Information and opinions are subject to change after the publication of this report, possibly rendering them inaccurate and/or incomplete.

Any unauthorised copying, alteration, distribution, transmission, performance, or display of this report, is prohibited.